The rapid growth of digital currencies has brought both opportunities and challenges to Latin America and the Caribbean (LAC) countries. While crypto assets promise benefits such as financial inclusion and faster payments, they also pose risks, especially concerning domestic currency substitution. In this article, we will delve into the risks associated with stablecoins, particularly the threat they pose on domestic currencies, and discuss how Central Bank Digital Currencies (CBDCs) can mitigate them.

Understanding the Risks of Stablecoins

Stablecoins, a type of crypto asset designed to maintain a stable value relative to a specified asset, have gained quite a popularity in LAC countries according to a recent report from the International Monetary Fund (IMF). However, the agency warned that their widespread adoption could potentially lead to domestic currency substitution, where citizens abandon their national currencies in favor of stablecoins.

This presents a significant risk to the monetary stability and sovereignty of the countries involved. The related concerns raised include reduced control over the money supply, potential disruption to monetary policy, and the erosion of trust in the domestic currency.

The Case of Meta’s Pilot Project

The experience of Meta’s pilot project in the United States and Guatemala is used by the IMF to illustrate the challenges of effective stablecoin adoption. While the said project aimed to facilitate cross-border payments without fees, it also carried the risk of domestic currency substitution in Guatemala.

Regulatory pushback eventually led to the project’s closure in 2022, highlighting the need for caution when considering stablecoin adoption in a macro setting.

The Promise of CBDCs

CBDCs have emerged as a potential solution to address the risks associated with stablecoins. These digital currencies issued by central banks, if well-designed, can offer increased usability, resilience, and efficiency in payment systems, while also fostering financial inclusion.

By integrating unbanked individuals and curbing currency substitution towards stablecoins or crypto assets, CBDCs can help preserve monetary sovereignty.

Enhancing Payment Systems and Financial Inclusion

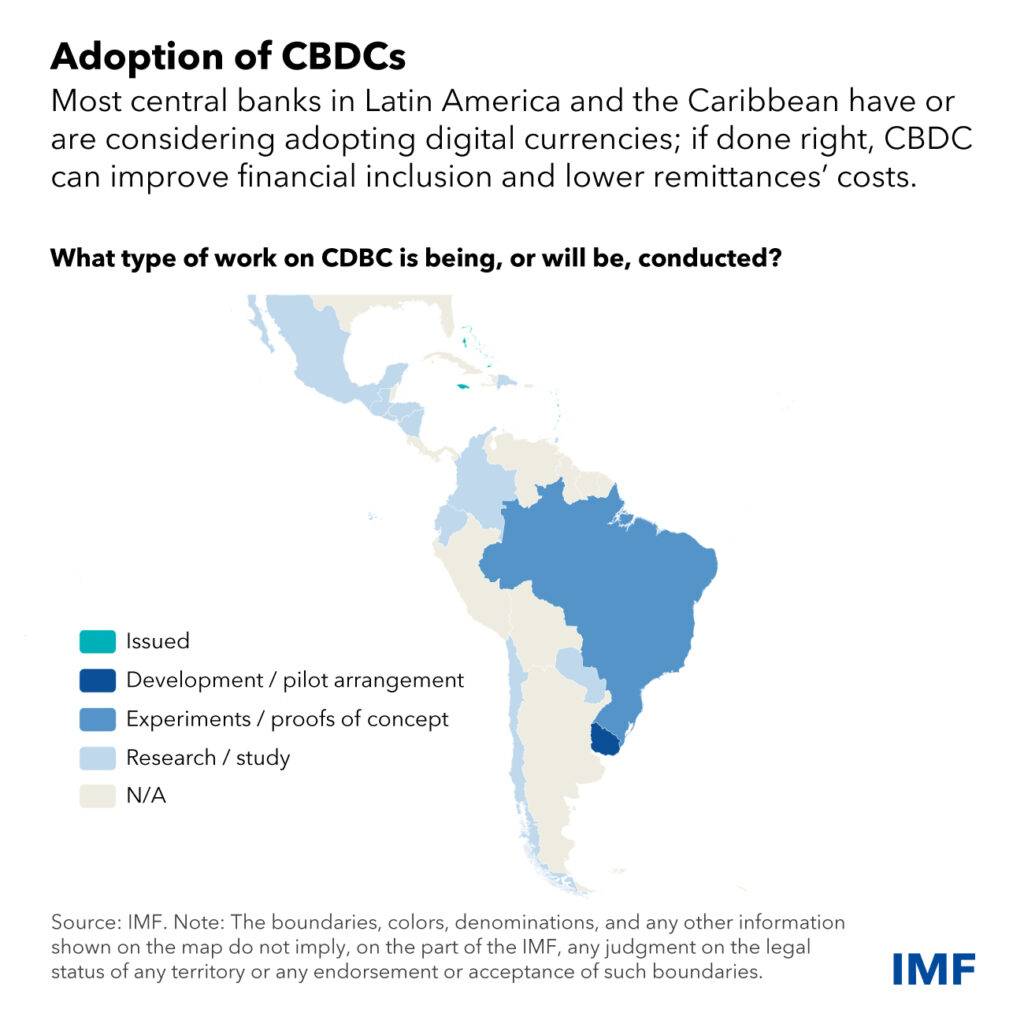

Most central banks in LAC are actively exploring the introduction of CBDCs based on the IMF’s findings. These central bank-issued digital currencies can enhance payment systems, making them more accessible and efficient for individuals and businesses alike.

Additionally, CBDCs can bridge the gap of financial inclusion by providing access to banking services for the unbanked population, ultimately reducing their reliance on unstable crypto assets.

Mitigating Risks and Ensuring Adoption

To ensure successful adoption and mitigate risks, LAC countries are recommended to invest in public awareness and robust infrastructure for CBDC implementation. Promoting transparency is crucial, as tracking and recording crypto asset transactions in national statistics can provide valuable insights into the demand for digital payment solutions.

Likewise, it is important for policymakers to address the underlying factors driving the demand for crypto assets, such as citizens’ unmet digital payment needs.

Final Thoughts

As Latin America and the Caribbean navigate the evolving landscape of digital currencies, the risks associated with stablecoins and domestic currency substitution require careful consideration. CBDCs offer a promising avenue to enhance payment systems, promote financial inclusion, and safeguard against the potential pitfalls of unregulated crypto assets.

By striking a balance between innovation and regulation, LAC countries can harness the benefits of digital currencies while protecting their monetary stability and sovereignty along the way.

{kind=link}