As the world watches in anticipation, central banks are quietly working behind the scenes on the design of their digital currencies. These currencies hold the key to unlocking a future that could be either a utopia or a dystopia.

But as authorities downplay what is happening, the question remains: Will they pave the way for a future where technology empowers citizens, or will they set the stage for a world where they track and monitor our every move? The fate of our digital future hangs in the balance.

What are Central Bank Digital Currencies?

CBDCs, or Central Bank Digital Currencies, are a new form of digital money that is issued by the central bank rather than private institutions like banks. CBDCs are also interchangeable with cash and can coexist with it.

European Central Bank (ECB) Goes “full steam ahead” with their CBDC

The digital Euro aims to keep pace with technology to meet market needs. It will have features such as programmability, controls on money exchange, different interest rates, and transaction limits during crises. Additionally, users will have a maximum amount that they can hold without additional cost. This will not, in any way, promote financial freedom.

For instance, Fabio Panetta, a Member of the Executive Board of the ECB suggests a maximum of 3,000-4,000 Euros per person without restrictive measures such as negative interest rates will be the standard allowance.

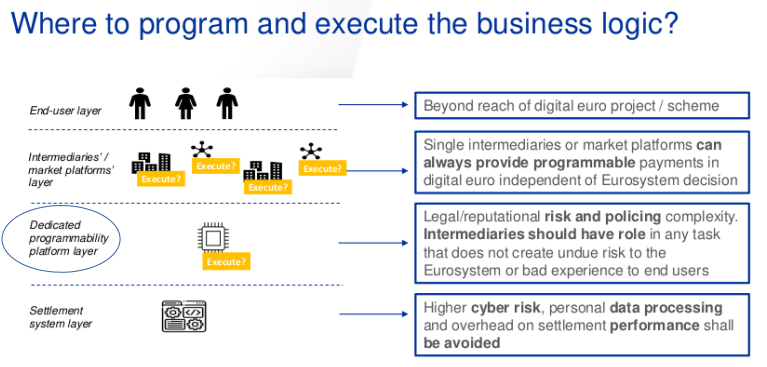

The ECB is creating both token and account-based systems for the digital Euro. The token system is less preferred as it takes away control from the ECB, while the account-based system is similar to the current banking system and is the preferred option of the ECB.

Financial service providers are already working on this system. Additionally, an EU-wide digital ID is also undergoing development alongside the digital Euro to facilitate transactions and other services under the eIDAS regulation.

On December 7, 2022, the ECB released a package (including letters that confirm the design choices) for financial intermediaries to begin building applications for the digital Euro.

Here are some of the conclusions drawn from the annex of the article:

- The digital Euro system will have intermediaries handle client interactions and the ECB will settle all transactions.

- The ECB will have the ultimate authority in approving or rejecting payments by responding with “SETTLED” or “FAILED” to every payment request.

- A permanent record of all transactions will always exist on the CBDC blockchain, disguised as ‘safeguarding privacy, and the ECB will use it to monitor an track your every move.

Conclusion

In conclusion, the move to digital payments reduces privacy and the ECB’s design for the digital Euro will allow the Eurosystem to view a minimum amount of transaction data. Privacy is okay for some low-value payments and offline transactions, but high-value transactions will still be subject to standard controls.

{kind=link}