As the world moves towards a more interconnected digital landscape, the banking industry is faced with the pressing need to adapt and engage with the rising generation of digital natives. Web 3.0, with its emphasis on decentralization, community building, and emerging technologies like non-fungible tokens (NFTs), presents a unique opportunity for banks to bridge the gap and attract these tech-savvy individuals as clients. But how does banking and Web3 fit together?

In this article, we explore how banks can leverage Web 3.0 and harness the value of NFTs to build communities, generate revenue, and retain digital natives as valuable customers.

What is Web 3.0?

Tim Berners-Lee pioneered the internet in 1990, he was a computer scientist at CERN, in the suburb of Geneva, Switzerland. This was the beginning of web 1.0, static website. Then web 2.0 came, driven by key innovations such as mobile internet access and social networks where people could share their content. In Web 3.0, applications and services are built on decentralized protocols and smart contracts, allowing for greater transparency, security, and trust. It enables peer-to-peer interactions without relying on intermediaries, and it empowers users by giving them ownership and control over their data. This decentralized and user-centric approach aims to foster innovation, privacy, and individual sovereignty on the internet.

What are NFTs

NFTs (non-fungible tokens) are unique cryptographic tokens that exist on a blockchain and cannot be replicated. On the other hand, crypto currencies are fungible. NFTs can represent digital or real-world items like artwork and real estate. To get more information about NFTs, just follow the NFT Think Tank.

“Tokenizing” these real-world tangible assets makes it very easy to buy, sell and trade them more efficient and reduce the probability of fraud. It is also very good described as ORB – Ownership Registered on the Blockchain.

Banking and Web3

Let us deep dive into how banks can use Web3 to attract GenZ?

Digital natives and Gen Z

A digital native is a person who grew up with the presence of digital technology or in the information age. They are comfortable with technology and it is part of their daily life. In general they are born after 1980, people born before and using technology like the digital natives, are digital immigrants. People born before 1980 are known for being hesitant to learn using new technology.

Gen Z’s behaviors are shaped by how they grew up, with climate change, pandemic lockdowns, and fears of economic collapse. They are born between 2000 – 2020. Gen Z or called Zoomers, are known for working, shopping, dating, and making friends online. In Asia, Gen Z spends six or more hours per day on their phones.

The great wealth transfer

In the next 2 decades, $84.4 trillion will be transferred to the younger generation, digital natives and Gen Z. This will drastically shake up the financial services industry as players – who are aware of it and get prepared – hunt for position with beneficiaries. To handle this from receiver side and banking side, technology will be integral and highly needed. Large banks have budget and invest in Fintech to get this managed and onboard the young generation. But this is only the technical side, the big quest is, how to attract them, how to integrate them and make them part of the community.

The consumer takes center stage

Based on a presentation by Ms. Maria von Scheel-Plessen, Gucci, the consumer is in the center of interest. In the old economy, the product was in the center of interest, now the time has changed and there are many similar products available, the consumer can select and if he is not happy, a change is quickly made. The next hull around the consumer is the experience,

How Web 3.0 will affect our life

Web 3.0, also known as the decentralized web, has the potential to significantly impact various aspects of our lives. While the exact details and implementation of Web 3.0 are still being developed, here are some potential ways it could affect us.

Web 3.0 is closely associated with blockchain technology and cryptocurrencies. Blockchain can enable transparent and tamper-resistant transactions, smart contracts, and decentralized applications (dApps). This may revolutionize finance, supply chain management, voting systems, and various other industries.

Personalized experiences: With Web 3.0, individuals may have more control over their online experiences. They can own their data and selectively share it with services or platforms of their choice. This could lead to more personalized and tailored interactions with websites and applications.

Enhanced digital identity: Web 3.0 could offer improved digital identity systems that are more secure, portable, and user-centric. Individuals may have better control over their online identities, reducing the risks of identity theft and fraud. In my opinion, the enhanced digital identity will change our life most.

Internet of Things (IoT): Web 3.0 can facilitate the integration of IoT devices by leveraging decentralized protocols. This may lead to more seamless and secure interactions between connected devices, enabling automation, improved data sharing, and new applications across various industries.

Content creation and ownership: Web 3.0 can empower content creators by enabling direct interactions with their audiences and facilitating peer-to-peer transactions. Artists, musicians, writers, and other creators may have more control over their work, monetization models, and copyrights.

Collaboration and sharing economy: Decentralized platforms and smart contracts can facilitate peer-to-peer collaboration and the sharing economy. Web 3.0 may enable trustless interactions, eliminating the need for intermediaries in areas like ride-sharing, home-sharing, freelancing, and crowdfunding.

How Web 3.0 will affect banking

These are the main points which I presented at the Richmond Financial Industry Forum in Interlaken, May 2023. Web 3.0, also known as the decentralized web, is an emerging paradigm that aims to transform the way information is stored, shared, and accessed on the internet. It encompasses various technologies such as blockchain, decentralized applications (dApps), smart contracts, and more. While it is difficult to predict the exact impact of Web 3.0 on the banking industry, there are several potential ways it could affect it:

1.Disintermediation

Web 3.0 has the potential to remove intermediaries, such as traditional banks, from certain financial transactions. Through the use of smart contracts on blockchain platforms, individuals and businesses can directly engage in peer-to-peer transactions without the need for intermediaries. This could reduce the need for traditional banking services in certain areas, such as remittances, international transfers, and decentralized lending.

2. Financial Inclusion

Web 3.0 technologies can enable greater financial inclusion by providing access to financial services for the unbanked and underbanked populations. Through decentralized applications, individuals can have access to banking-like services, such as savings, loans, and payments, using just a smartphone and internet connection. This can help empower individuals in underserved regions and bridge the global financial inclusion gap.

3. Tokenization and Digital Assets

Web 3.0 enables the tokenization of assets, where physical or digital assets can be represented as blockchain-based tokens. This opens up new possibilities for banking, such as fractional ownership of assets, tokenized securities, and new forms of fundraising through Initial Coin Offerings (ICOs) or Security Token Offerings (STOs). Banks could adapt their services to support the issuance, trading, and custody of digital assets.

4. Enhanced Security and Privacy

Web 3.0 technologies can improve the security and privacy of financial transactions. Blockchain, with its decentralized and immutable nature, can make transactions more secure and transparent. Additionally, users have greater control over their personal data and can choose to share only the necessary information for specific transactions, reducing the risk of data breaches.

5. Regulatory Challenges

As Web 3.0 evolves, regulators and policymakers will need to adapt to the changing landscape. The decentralized nature of Web 3.0 can present challenges in terms of oversight, consumer protection, and compliance with existing financial regulations. Regulators will need to strike a balance between fostering innovation and ensuring stability and security in the banking sector.

It’s important to note that Web 3.0 is still in its early stages, and its full impact on the banking industry is yet to be realized. The extent of its influence will depend on the adoption of Web 3.0 technologies, regulatory developments, and the ability of banks to adapt and leverage the potential benefits offered by this new paradigm.

Banks already using Web 3.0

That web 3.0 is loved by digital natives it offers huge potential for banking industry.

What are the advantages for banks using Web 3.0 vs. Web 2.0?

Web 3.0 offers several potential advantages for banks compared to the traditional Web 2.0 model. Here are some of the advantages that banks can leverage with Web 3.0:

1. Enhanced Security

Web 3.0 technologies, such as blockchain, provide stronger security mechanisms compared to Web 2.0. The decentralized and immutable nature of blockchain can help prevent unauthorized tampering or manipulation of financial data, reducing the risk of fraud. Banks can benefit from increased trust and transparency in transactions, improving overall security for their customers.

2. Cost Reduction

Web 3.0 can potentially help banks reduce operational costs. By leveraging decentralized systems, banks can eliminate or minimize the need for intermediaries and associated fees. Smart contracts on blockchain platforms can automate certain processes, reducing manual effort and overhead costs. Additionally, Web 3.0 can enable faster and more efficient cross-border transactions, potentially reducing costs associated with international transfers.

3. Improved Efficiency and Speed

Web 3.0 technologies offer the potential for faster and more efficient financial transactions. Blockchain-based systems can facilitate near-instantaneous settlement, eliminating the need for traditional clearinghouses or lengthy reconciliation processes. This can improve liquidity management for banks and enable real-time transactions, enhancing the overall efficiency of their operations.

4. Expanded Market Opportunities

Web 3.0 opens up new market opportunities for banks. By embracing digital assets and tokenization, banks can participate in the growing ecosystem of decentralized finance (DeFi). They can offer services related to digital assets, such as custody, trading, and investment management. Additionally, banks can explore partnerships with fintech startups leveraging Web 3.0 technologies to offer innovative financial products and services.

5. Enhanced Customer Experience

Web 3.0 can enable a more personalized and user-centric banking experience. Through decentralized applications and smart contracts, banks can offer customized financial solutions to their customers, tailored to their specific needs and preferences. Customers can have greater control over their financial data and choose which institutions or applications can access it, enhancing privacy and empowering individuals in their financial decisions.

It’s important to note that the advantages of Web 3.0 for banks are contingent upon the successful adoption and integration of these technologies into their existing infrastructure. Banks would need to navigate regulatory challenges, address scalability issues, and ensure interoperability with legacy systems to fully leverage the potential benefits of Web 3.0.

Use-cases in Web 3.0 banking

This is a partial list of use-cases shows that Web 3.0 is great and you can solve a lot of issues with it within the banking system.

- American Express “The Loft”

- JP Morgan – JPM Coin

- HSBC virtual global trade finance platform

- Bank of HODL – Decentraland

- Somnium Financial – Somnium Space

- BlockFi – Cryptovoxels

- Bitwage – Decentraland

- Nebeus – Somnium Space

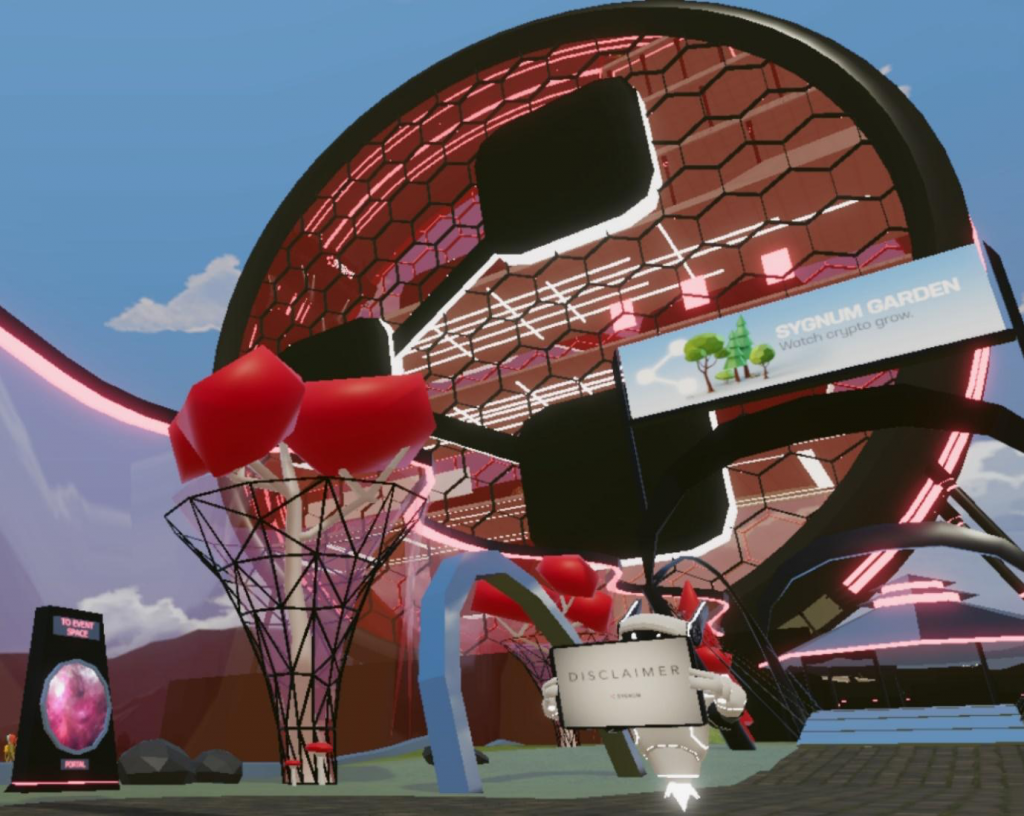

- Sygnum – Decentraland

For example, JP Morgan was fighting in the past against cryptocurrency, but already 2019 they launched the JPM Coin which is the answer to the SWIFT payment system, featuring smaller costs, much faster settlement times as well as reduced error margins. Sygnum Bank has a land parcel on Decentraland, located at (-7/12), features a CryptoPunk receptionist, an interactive NFT gallery and event space.

How do NFTs affect banks?

NFTs (Non-Fungible Tokens) have gained significant attention in recent years as a technology that can be used to represent ownership or authenticity of unique digital assets. While NFTs have primarily been associated with art, collectibles, and digital assets, there are potential use cases for NFTs in the banking industry as well. Here are a few ways NFTs could potentially help banks:

- Tokenizing Assets

- Digital Identity Verification

- Proof of Authenticity

- Loyalty Programs

- Art Finance

The banks are exploring various applications. While there are opportunities, there are also challenges, such as regulatory considerations, scalability, and interoperability. The integration of NFTs into banking systems would require careful consideration of these factors. But it is essential to integrate NFTs in any way, not to miss getting a piece of the big wealth transfer.

The benefits of transforming banks with Web3

The rise of digital natives, who are individuals born and raised in the digital age, has indeed brought significant changes to consumer expectations and behaviors. To remain relevant and competitive in this evolving landscape, banks will need to undergo a transformation to meet the needs and preferences of this new generation. Digital natives expect seamless, intuitive, and personalized digital experiences across various devices. Banks need to invest in user-friendly online and mobile banking platforms, offering features such as real-time notifications, easy fund transfers, and intuitive account management. They are heavily relying on smartphones for their everyday activities, banks should prioritize mobile banking experiences.

Open Banking initiatives allow banks to securely share customer data with third-party providers through APIs (Application Programming Interfaces). Embracing open banking can enable banks to offer customers a broader range of services and foster innovation through partnerships with fintech companies, providing digital natives with a more comprehensive and tailored financial ecosystem. The transformation required will vary for each bank, but the overarching goal is to create a customer-centric, digitally-driven banking experience that resonates with the preferences and expectations of digital natives.

Actionlist for tomorrow

In the chapters above everything is described what banks need to move into Web3, but here is a summary of all the steps needed to be successful.

- Check the behavior of your clients and prospects

- Implement a NFT strategy

- Either start with membership to engage the clients and prospects in a community, or

- Fractionalize assets

This are great ways to get experience and get quick results and feedback. When you have gained experience and adapted your mindset in the entire bank to be successful in the future, you can try the next steps.

Both ways are a great way to be successful, but you must start now!

For more information on Banking and Web3, please feel free to reach out to me at [email protected]

{kind=link}